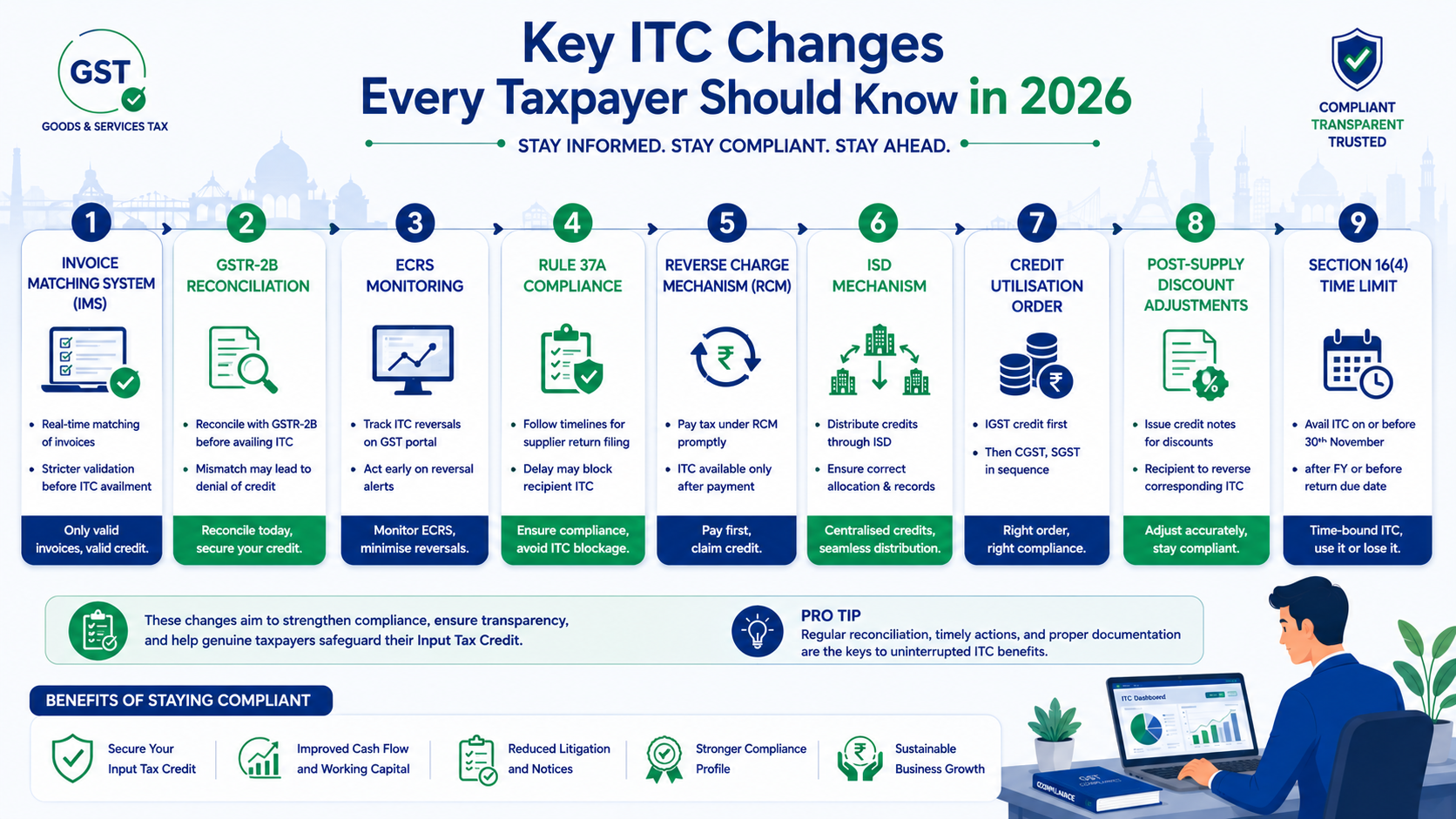

Input Tax Credit (ITC) continues to be the backbone of the GST system. In 2026, the government has introduced several major changes through technology upgrades and amendments to strengthen compliance and prevent misuse. This article provides a detailed analysis of the key updates.

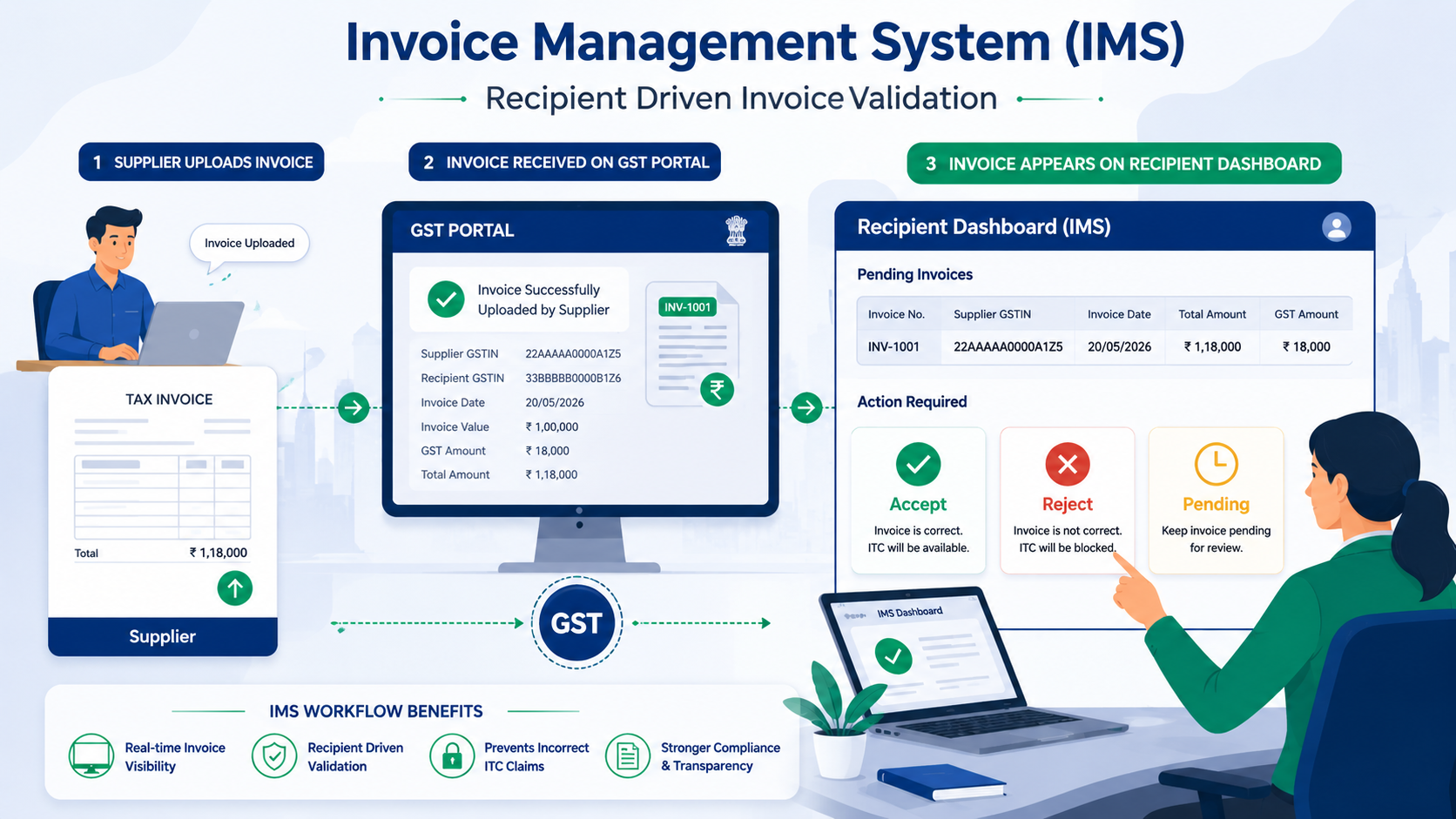

1. Invoice Management System (IMS) – A New Era of ITC Verification

The Invoice Management System (IMS) has become operational under Section 38 of the CGST Act. Every invoice uploaded by the supplier in GSTR-1 is now visible to the recipient for acceptance, rejection, or keeping pending.

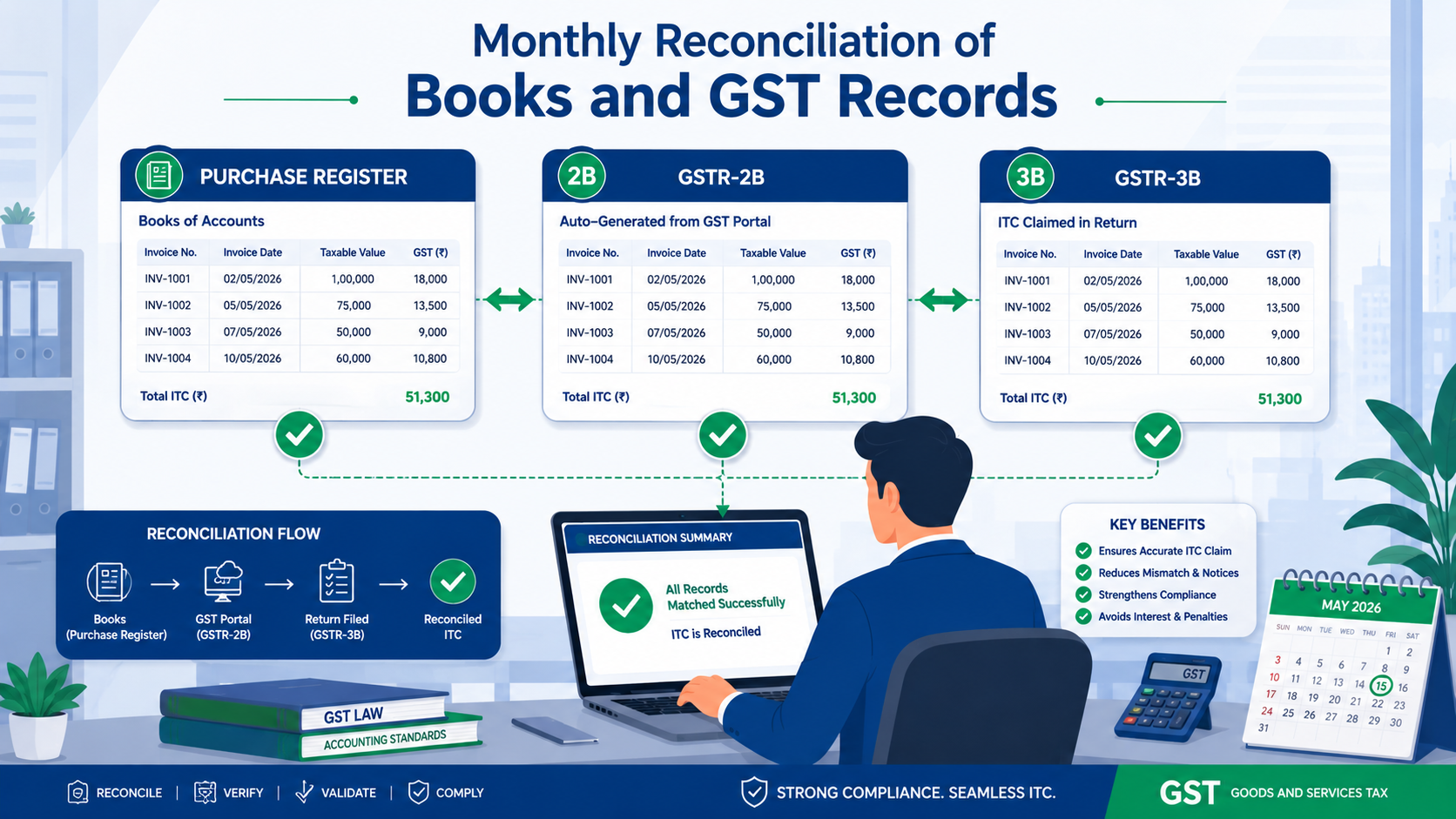

2. GSTR-2B Reconciliation Becomes Mandatory in Practice

As per Section 16(2)(aa), ITC can be availed only when the supplier has furnished the invoice details in GSTR-1 and they are communicated to the recipient via GSTR-2B.

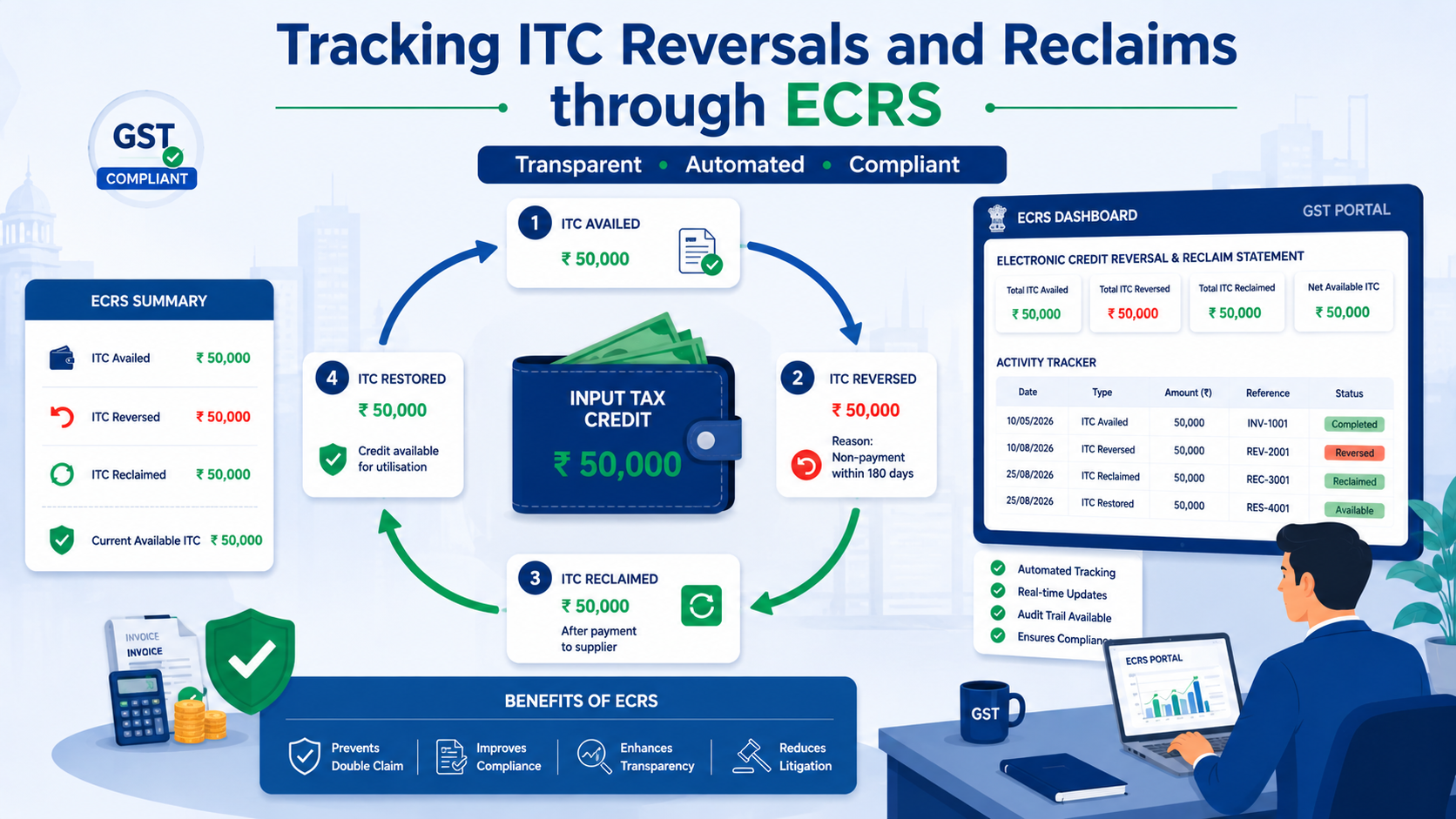

3. Electronic Credit Reversal and Reclaimed Statement (ECRS)

The portal now electronically tracks ITC reversals and reclaims under Rules 37, 42 & 43 to prevent double claims.

4. Rule 37A – Monitoring Supplier Compliance

Recipients must now monitor whether their suppliers have filed GSTR-3B. Failure by the supplier may require reversal of ITC by the recipient.

5. Reverse Charge Mechanism (RCM) and ITC

ITC on RCM supplies can be claimed only after payment of tax under reverse charge.

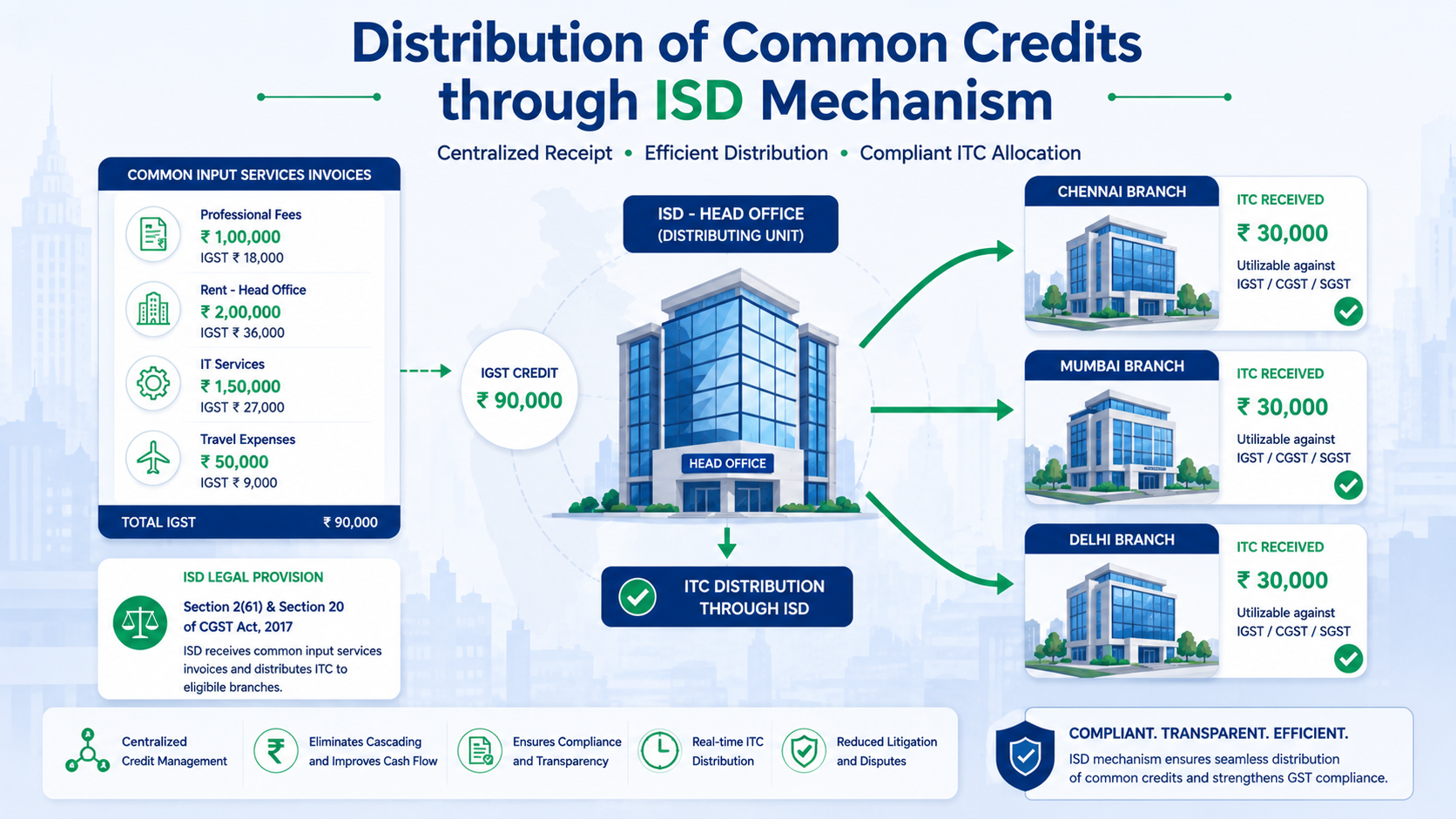

6. Expansion of Input Service Distributor (ISD) Framework

The ISD mechanism has been strengthened to distribute RCM credits as well, bringing more clarity for head offices.

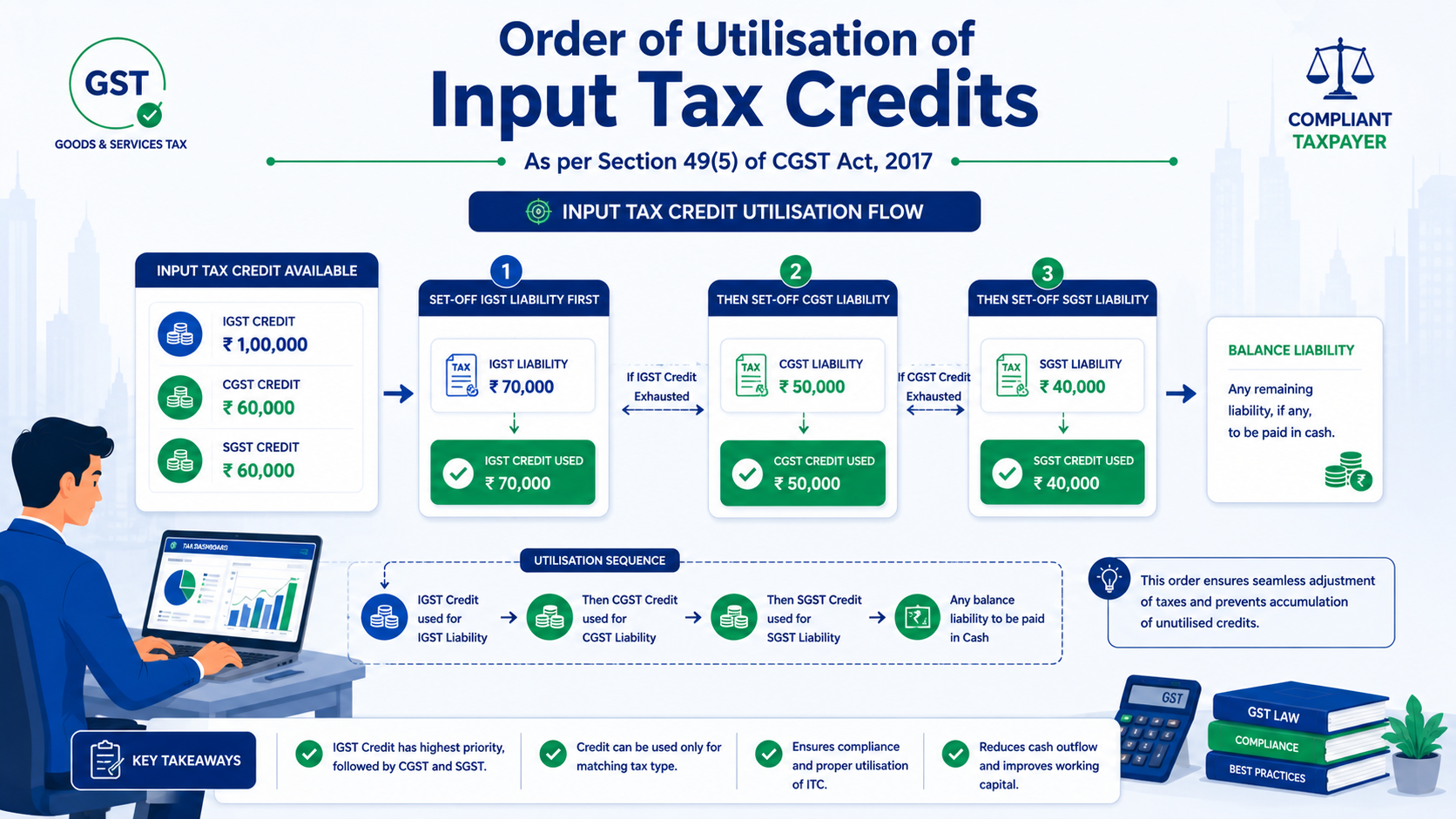

7. New ITC Utilisation Sequence

Greater flexibility has been introduced in utilising CGST/SGST credit against IGST liability after mandatory adjustments.

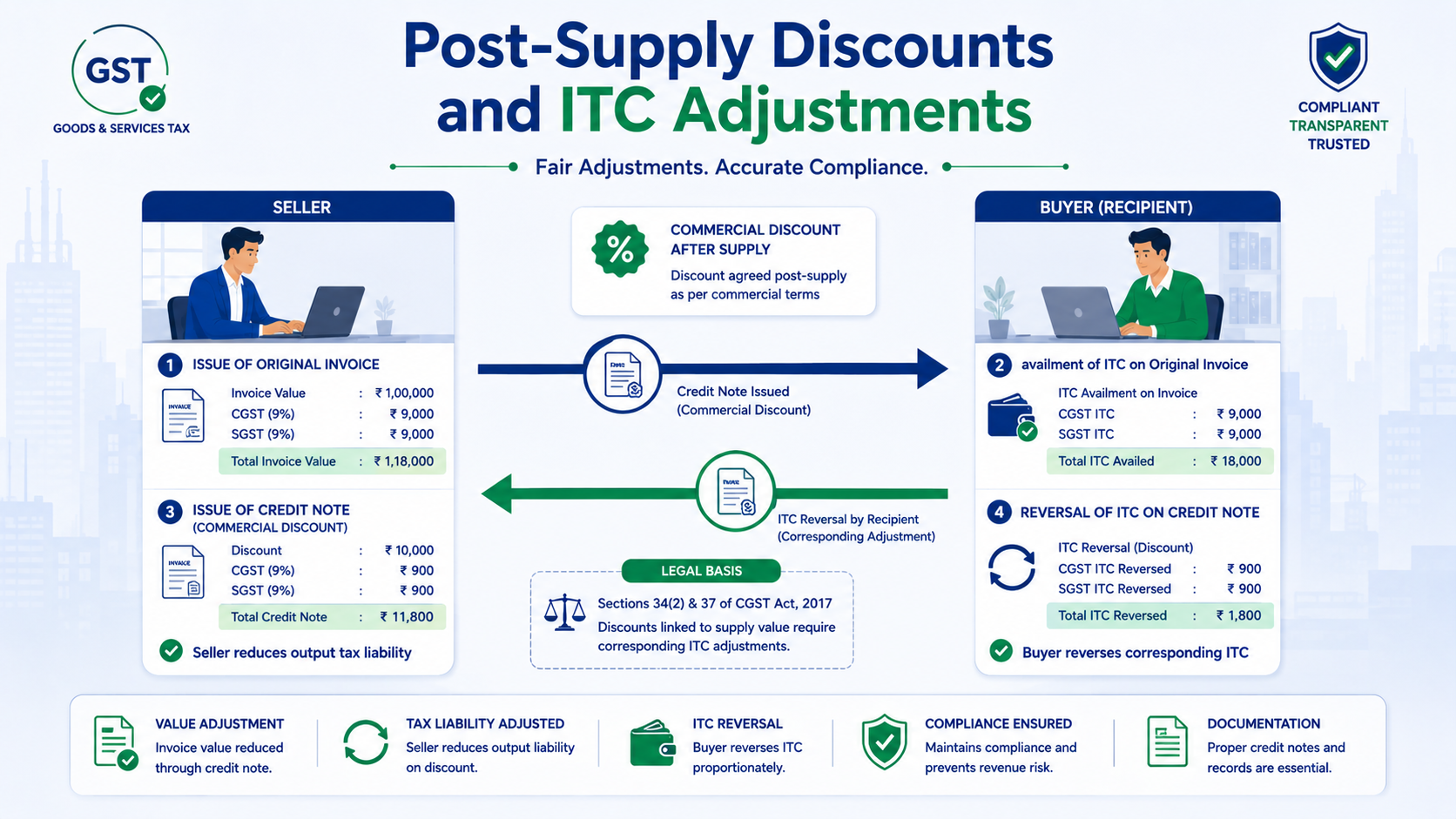

8. ITC and Post-Supply Discounts

Proposed relaxation allows deduction of post-supply discounts even without prior agreement, subject to conditions and ITC reversal by the recipient.

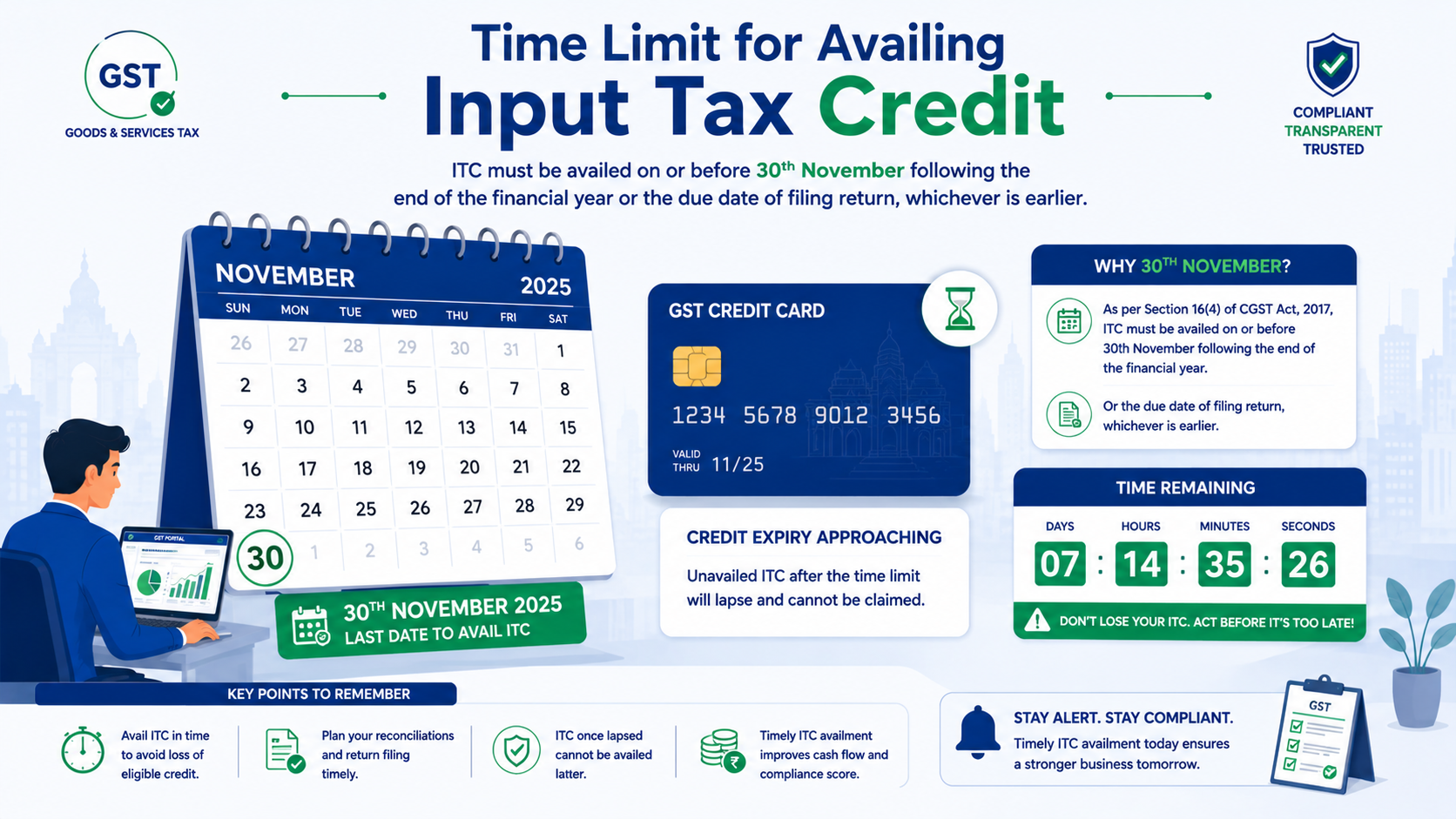

9. ITC Time Limit – Section 16(4)

ITC must be claimed by 30th November following the end of the financial year or the date of filing the annual return, whichever is earlier.

Key Takeaways for Businesses

- •Monthly IMS actions are now critical for ITC eligibility.

- •GSTR-2B reconciliation is mandatory in practice.

- •Monitor supplier compliance under Rule 37A.

- •Pay RCM tax before claiming ITC.

- •Track reversals and reclaims through ECRS.

- •Do not miss the Section 16(4) deadline.

Conclusion

GST compliance in 2026 has become more technology-driven. Businesses and professionals must adapt quickly to the new systems like IMS, ECRS, and stricter reconciliation requirements to avoid disputes and interest liabilities.

Written by Vignesh VR on June 02, 2026

Category: GST